Real Estate Market Statistics around Winnipeg and Surrounding Areas for March 2026

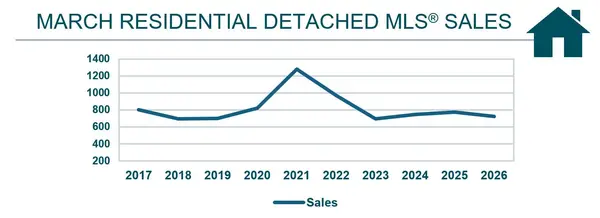

Real Estate Market Statistics around Winnipeg and Surrounding Areas for March 2026 The March 2026 real estate market in Winnipeg and surrounding areas shows a shift toward more balanced conditions. While sales and listings have declined, prices remain strong — highlighting a market driven by limited

Real Estate Market Statistics around Winnipeg and Surrounding Areas for February 2026

Winnipeg Real Estate Market Update for February 2026 Condo Prices Hit Record February High as Winnipeg Housing Market Stabilizes The Winnipeg real estate market in February 2026 showed signs of stabilization as sales slowed compared to last year but home prices remained resilient. While detached hom

Common Property Title Procedures and Issues When Buying or Selling a Home

Oversight of Manitoba’s Land Registration System The land registration system is overseen by the Manitoba Registrar-General , a lawyer appointed under The Public Service Act and a member of the Law Society of Manitoba. The Registrar-General provides oversight of the province’s land titles and perso

Tara Zacharias

Phone:+1(204) 293-0933