10 Steps to Getting Pre-Approved for a Mortgage in Manitoba

Securing a loan approval for a mortgage in Winnipeg involves a series of steps and considerations to ensure you meet the lender's requirements and get the best possible terms.

Here's a comprehensive guide to navigating the mortgage approval process.

-

Understand Your Financial Situation - Review credit score, income, and debt-to-income ratio.

-

Determine Your Budget - Calculate affordability and save for a suitable down payment.

-

Choose the Right Mortgage - Decide between fixed/variable rates, mortgage term, and amortization.

-

Gather Necessary Documentation - Collect ID, income proof, asset documents, and credit report.

-

Get Pre-Approved - Apply for pre-approval to estimate borrowing capacity.

-

Apply for a Mortgage - Choose a lender, submit your application and documents.

-

Mortgage Underwriting - Underwriters review your credit, financials, and risk profile.

-

Conditional Approval - Meet additional requirements like appraisals or insurance if needed.

-

Final Approval and Closing - Complete final paperwork and pay closing costs to secure mortgage.

-

Post-Approval - Set up payment schedule and review mortgage terms regularly.

10 Steps to Getting Pre-approved for a Mortgage in Manitoba

1. Understand Your Financial Situation

- Credit Score: Check your credit score before applying. A higher score generally improves your chances of getting a mortgage with favourable terms. In Canada, scores above 650 are considered good, but higher scores can offer better rates.

- Credit Card Debt: Reduce your amount owing prior to application to improve your credit score and balance your debt-to-income ratio.

- Income and Employment: Ensure you have stable and sufficient income. Lenders typically require proof of employment and income, such as recent pay stubs, two years of tax returns, or a letter from your employer.

- Debt-to-Income Ratio: Calculate your debt-to-income ratio (DTI), which is the percentage of your gross monthly income (your pay before taxes and other deductions are taken out) that goes towards paying your monthly debt payments. Lenders use this ratio to assess your ability to manage mortgage payments alongside other debts, this determines your borrowing risk. A DTI of less than 36% is considered a healthy one.

2. Determine Your Budget

- Affordability: Use a mortgage calculator to estimate how much you can afford to borrow based on your income, expenses, and current interest rates.

- Down Payment: Save for a down payment. In Canada, the minimum down payment is 5% for homes costing up to $500,000 and 10% for the portion of the price above $500,000. For properties over $1 million, the minimum is 20%. A higher down payment is considered advantageous when there is competition during the situation of multiple offers.

3. Choose the Right Mortgage

- Fixed vs. Variable Rates: Decide between a fixed-rate mortgage, where the interest rate stays the same for the term, or a variable-rate mortgage, where the rate can fluctuate with the market.

- Mortgage Term: Select the term of your mortgage, which can range from a few months to 5 years or more. Less than 5 years is a short-term mortgage, more than 5 years is a long-term mortgage. Your lender may move your short-term mortgage to a long-term mortgage to make this a convertible term mortgage which will reflect a new interest rate. At the end of each term you will need to renew your mortgage. This could likely take a few terms to repay the mortgage. Shorter terms usually have higher monthly payments but lower total interest costs, while longer terms offer lower monthly payments.

- Amortization Period: In consideration with the mortgage term, the amortization period will impact your overall costs, interest rates and the amount of your regular payments. The amortization period is the overall length of time you will have to pay the mortgage in full. The longer the amortization period, the lower your payments. However, by taking a longer time to pay the mortgage you will be paying more in interest.

4. Gather Necessary Documentation

- Identification: Provide proof of identity, such as a driver’s license or passport. Have at least two pieces of identification, with at least one to be government issued photo ID.

- Proof of Income: Submit recent pay stubs, tax returns, or financial statements if self-employed.

- Proof of Assets: Show evidence of your savings and other assets, such as bank statements and investment portfolios.

- Credit Report: Lenders will pull your credit report to review your credit history and score.

- Loan Agreements: If you lease or have borrowed any other money for purchases such as vehicles, boats, education etc. These documents should be available for the lender.

5. Get Pre-Approved

- Pre-Approval Process: Apply for pre-approval from a lender or mortgage broker. Pre-approval provides an estimate of how much you can borrow and can strengthen your position when making an offer on a home.

- Pre-Approval Letter: Obtain a pre-approval letter to show sellers that you are a serious buyer with the financial backing to make an offer.

6. Apply for a Mortgage

- Select a Lender: Choose a lender based on interest rates, fees, and customer service. Consider working with a mortgage broker who can help you find the best deal.

- Complete Application: Fill out the mortgage application form and submit all required documents. The lender will assess your application and may request additional information.

7. Mortgage Underwriting

- Underwriting Process: The lender’s underwriting department will review your application, credit history, and financial documents. They assess risk and ensure you meet the lender’s criteria.

- Additional Information: Be prepared to provide further documentation or clarification if requested by the underwriter.

8. Conditional Approval

- Approval Conditions: If your mortgage is conditionally approved, you may need to meet specific conditions before final approval, such as providing additional documentation or getting a property appraisal.

- Property Appraisal: The lender may require a professional appraisal to determine the market value of the property you wish to buy. This is an expense, not to be included in your down payment amount and may cost approximately $300, to be paid to your lender.

- Mortage Insurance: Canada Mortage and Housing Corporation (CMHC) insurance is required on all homes with less than 20% down payment of the purchase price. This protects lenders against mortgage default and enables consumers to purchase with a minimum down payment starting at 5%. Your lender pays this premium, which can be paid in one lump sum or added to your monthly mortgage payments.

9. Final Approval and Closing

- Final Approval: Once all conditions are met, and the lender is satisfied with the appraisal and documentation, you will receive final approval.

- Closing Process: Work with your real estate agent and lawyer to finalize the purchase. Review and sign closing documents and arrange for the down payment and closing costs.

10. Post-Approval

- Mortgage Payments: Set up a payment schedule for your mortgage, ensuring you understand your payment due dates and amounts.

- Review Terms: Regularly review your mortgage terms and consider refinancing options if interest rates drop or your financial situation changes.

Local Considerations for Winnipeg

- Property Taxes: Factor in local property taxes, which can vary by neighborhood and property value. In Winnipeg property tax can be paid monthly, instead of one lump sum in August, through the Tax Instalment Payment Plan (TIPP).

- Insurance Requirements: Ensure you have adequate homeowners insurance, including coverage for hazards common in Winnipeg, like winter-related damage. It is not legally required if you have paid your home in full, but recommended. If you are securing a mortgage through a lender, you will be required to have homeowners insurance.

By following these steps and understanding the requirements and options available, you can navigate the mortgage approval process effectively and secure a loan that meets your needs and financial goals.

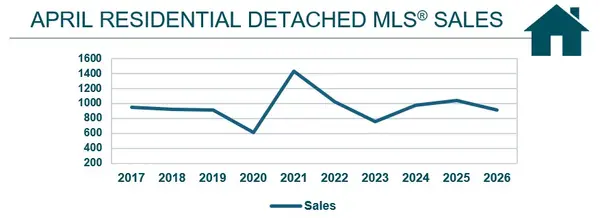

When to Get Pre-Approved for a Mortage

Categories

Recent Posts

Leave a Reply

REALTOR®

REALTOR®I became a REALTOR® because I truly enjoy helping people find the place that feels like home and because providing exceptional service during such an important moment in someone’s life is something I genuinely care about. Supporting sellers as they move on, move up, or move forward is just as meaningful, and being part of that transition is something I’m grateful to contribute to.

I make the buying or selling journey feel organized and approachable with clear communication and practical guidance. With an approach supported by market data, trends, and neighbourhood insights, you'll always understand what’s happening and how to make the most informed decisions.

Whether you’re buying your first home, selling a place filled with memories, or planning your next step, I’m here as someone who listens, shows up, and puts your goals at the centre of every decision. I'm focused on what serves you best and I make your best interests my TOP priority.

I'm Tara Zacharias, a real estate salesperson located in the vibrant city of Winnipeg. Thanks for stopping by and taking the time to get to know me!+1(204) 293-0933 tara@tarazacharias.com330 St Mary Ave, Winnipeg, MB, R3C 3Z5, CAN

https://tarazacharias.com/