The Bank of Canada, Interest Rates, and How They Affect Borrowers

by Tara Zacharias

Bank of Canada Head Office in Ottawa / Source: Bank of Canada

What is the Bank of Canada?

The Bank of Canada is the country’s central bank. It is not a commercial bank and does not lend to consumers or take deposits.

Its main roles include,

Setting the policy interest rate (also called the overnight rate) to control inflation and support economic stability.

Issuing Canada’s currency (the Canadian dollar).

Regulating the money supply and ensuring stable prices.

Overseeing the financial system to keep it safe and efficient.

Acting as a lender of last resort for major financial institutions during crises.

The Bank of Canada sets the economic framework that influences how much you pay to borrow money but it does not lend directly to individuals.

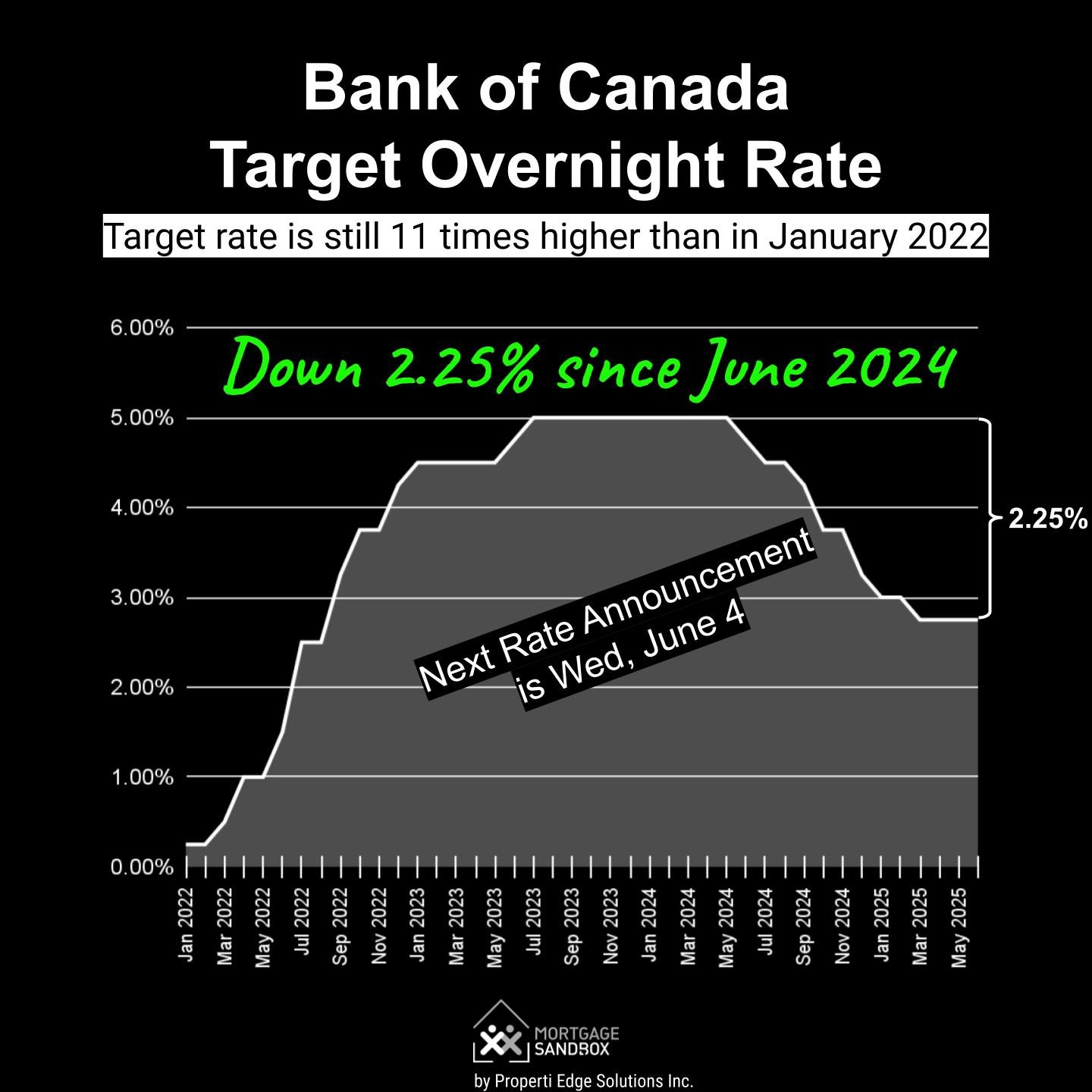

The Policy Interest Rate in Canada

The policy interest rate also called the overnight rate, this is the rate at which the Bank of Canada lends money to major financial institutions lend money overnight. It sets the baseline for how expensive it is to borrow money in Canada.

If the Bank raises the rate → borrowing becomes more expensive

If the Bank lowers the rate → borrowing becomes cheaper

If the Bank pauses→ the rate stays the same as before

When the Bank of Canada pauses its policy interest rate, it means the central bank has decided not to raise or lower the overnight lending rate (also called the policy rate) at that particular announcement.

A pause usually signals that the Bank,

Believes the current rate is appropriate to keep inflation under control

Wants more time to observe how previous rate changes are impacting the economy

Is uncertain about economic conditions and prefers to wait for more data

What Does a Pause Mean for Canadians?

For Homeowners & Buyers

No change to variable mortgage rates or lines of credit tied to the prime rate

Stabilized borrowing costs may offer breathing room for those with adjustable-rate mortgages

Fixed mortgage rates (tied to bond yields) might not move immediately but a pause could influence them over time

For Consumers

Credit card and personal loan interest rates may also stay stable

People may delay major purchases if they expect rates to fall later

For the Economy

A pause allows businesses and consumers to adjust to previous hikes

It may signal that inflation is starting to slow, or that growth is weakening

Who Are the Commercial Banks in Canada?

Commercial banks are financial institutions that serve the public directly. They accept deposits, offer savings and chequing accounts, and provide loans, mortgages, credit cards, and other financial products.

Major Commercial Banks in Canada (often called the "Big Six")

Royal Bank of Canada (RBC)

Toronto-Dominion Bank (TD Canada Trust)

Bank of Nova Scotia (Scotiabank)

Bank of Montreal (BMO)

Canadian Imperial Bank of Commerce (CIBC)

National Bank of Canada

Other institutions like Laurentian Bank, EQ Bank, Tangerine, and various credit unions also offer banking services to the public.

What is the Borrowing Rate from a Commercial Bank?

The prime rate is the benchmark interest rate that commercial banks charge their customers. It serves as a starting point for setting interest rates on a wide range of loans and credit products for both businesses and individuals.

Key Characteristics

Base for Variable Interest Rates - Many consumer and business loans, such as variable-rate mortgages, lines of credit, student loans, and auto loans, are tied to the prime rate. The interest charged is usually the prime rate plus a certain percentage (a "spread") based on the borrower’s risk profile.

Responsive to Central Bank Policy - The prime rate is heavily influenced by the central bank’s policy rate—in Canada, that’s the Bank of Canada (BoC) overnight rate. When the BoC adjusts its rate, commercial banks typically follow by adjusting the prime rate accordingly.

Uniform Among Major Banks - Although technically each bank sets its own prime rate, the rate tends to be identical across major institutions, reflecting coordinated responses to monetary policy.

The Prime Rate or Borrowing Rate

This is the interest rate that a bank charges you, a consumer or business, for

Mortgages

Personal loans

Credit cards

Business lines of credit

Understanding the difference between the key interest rate (also known as the policy rate) and the borrowing rate from a commercial bank is crucial for anyone managing a mortgage, loan, or investment.

This rate is

Based on the key interest rate, but includes a markup or spread to cover the bank’s costs and profit margin.

When the key rate changes, banks adjust their own prime rate (usually within a day or two).

The borrowing rate you see is tied to that prime rate, but varies by product and borrower risk.

Also influenced by other factors, such as,

Your credit score

Type and term of loan

Market competition

Bank’s internal lending policies

What Commercial Banks Do for Borrowers

Think of the Bank of Canada as the country’s financial steering wheel, it sets direction and pace. Commercial banks are the vehicle that carries you along the road, offering tools, credit, and access to the financial system.

1. Provide Access to Credit

Mortgages

Personal loans and lines of credit

Credit cards

Student loans

Business loans

2. Determine Lending Terms

They assess your,

Credit score

Income and employment history

Debt levels

Down payment (for mortgages)

Based on this, they decide,

How much you can borrow

Your interest rate

Loan terms and repayment schedule

3. Link to the Bank of Canada’s Policy Rate

Commercial banks use the Bank of Canada’s policy rate to set their own prime rate, which influences,

Profits are reinvested into the community or returned to members

Often more flexible lending criteria

Whether you're seeking a first mortgage, small business loan, or refinancing, credit unions can be an excellent alternative to the big banks, especially for Manitobans who value local decision-making and community impact.

Final Takeaway

Understanding the policy rate is more than just keeping up with financial headlines, it’s about knowing how The Bank of Canada’s decisions can impact your buying power, mortgage rates, and long-term real estate goals. Whether rates are rising, holding steady, or falling, staying informed helps you make confident decisions in a shifting market.

As a REALTOR®, I’m here to guide you through these financial dynamics with clarity and care. Whether you're planning to buy your first home, upgrade to a new space, or simply want to understand how current rates affect your property's value, I’m just a call away.

I became a REALTOR® because I truly enjoy helping people find the place that feels like home and because providing exceptional service during such an important moment in someone’s life is something I genuinely care about. Supporting sellers as they move on, move up, or move forward is just as meaningful, and being part of that transition is something I’m grateful to contribute to.

I make the buying or selling journey feel organized and approachable with clear communication and practical guidance. With an approach supported by market data, trends, and neighbourhood insights, you'll always understand what’s happening and how to make the most informed decisions.

Whether you’re buying your first home, selling a place filled with memories, or planning your next step, I’m here as someone who listens, shows up, and puts your goals at the centre of every decision. I'm focused on what serves you best and I make your best interests my TOP priority.

I'm Tara Zacharias, a real estate salesperson located in the vibrant city of Winnipeg. Thanks for stopping by and taking the time to get to know me!

REALTOR®

REALTOR®