Taxes, Rebates and Closing Costs When Buying an existing Home or New Build

Taxes, Rebates and Closing Costs When Buying a Home in Canada Buying a home comes with more than just a down payment and mortgage approval. Whether you’re purchasing your first home, upgrading to a larger property, buying a newly built home or investing in real estate, understanding taxes and reba

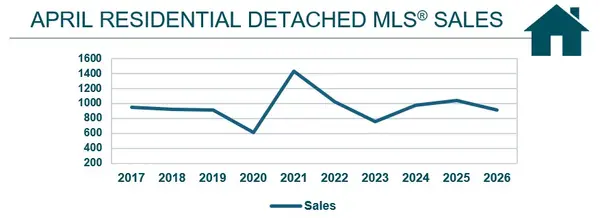

Real Estate Market Statistics around Winnipeg and Surrounding Areas for April 2026

Winnipeg and Surrounding Areas Real Estate Market Update – April 2026 The Winnipeg real estate market continued to show resilience through April 2026, with home prices climbing across most property categories despite softer sales activity compared to last year’s near-record pace. While buyers are se

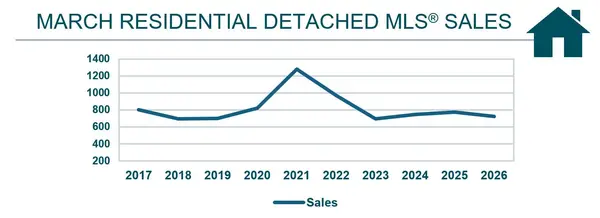

Real Estate Market Statistics around Winnipeg and Surrounding Areas for March 2026

Real Estate Market Statistics around Winnipeg and Surrounding Areas for March 2026 The March 2026 real estate market in Winnipeg and surrounding areas shows a shift toward more balanced conditions. While sales and listings have declined, prices remain strong — highlighting a market driven by limited

Tara Zacharias

Phone:+1(204) 293-0933