8 First-Time Home Buyer Programs and Incentives for Manitoba Residents

-

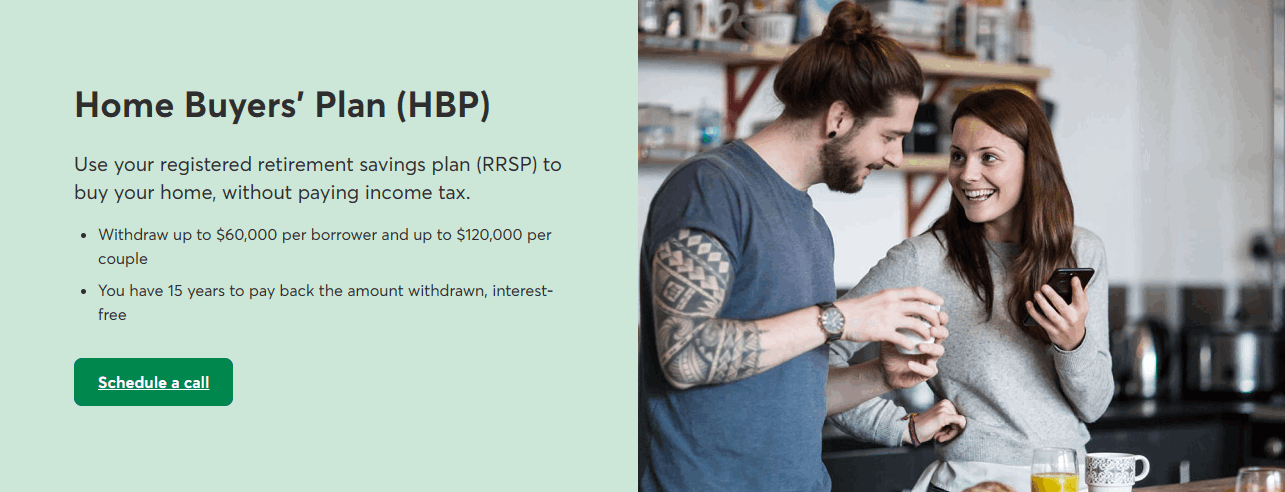

Home Buyers' Plan (HBP): Withdraw RRSP funds, tax-free, to put towards a first home purchase.

-

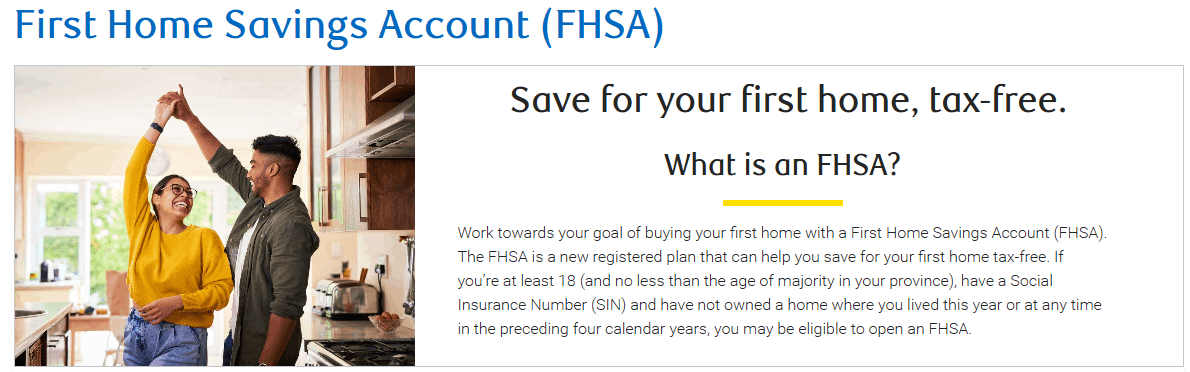

First Home Savings Account (FHSA): Tax-free savings account for a first home down payment.

-

First-Time Home Buyers’ Tax Credit (HBTC): Claim a tax credit to offset purchase costs.

-

GST/HST New Housing Rebate: Recover part of GST or HST on a new home build.

- First-Time Homebuyers' GST Rebate on a new home build.

-

First Time Home Purchase Program (FTHPP): For Metis citizens who are first-time home buyers to assist with down payment and closing costs.

-

Rural HomeOwnership Program (RHP): Provides affordable homeownership through Manitoba Housing in rural areas.

-

Manitoba Tipi Matawa Program (MTM): A Manitoban First Nations, first-time homebuyers' program that is designed to help with down payment, while providing home-purchase education.

8 First-Time Home Buyer Programs Available in Manitoba

When buying your first home, you might be surprised by the additional costs beyond your down payment.

Expenses like moving fees, legal costs, inspections, and taxes can quickly add up, sometimes catching new buyers off guard. Fortunately, first-time homebuyers in Canada have access to programs designed to offset these costs, making homeownership more accessible.

Here’s an overview of valuable programs available for first-time homebuyers in Manitoba.

1. Home Buyers’ Plan (HBP)

Overview

Requirements

Requirements include being a first-time buyer and intending to use the home as your principal residence within one year. You must repay the loan within 15 years to avoid penalties, starting the second year after withdrawal.

2. First Home Savings Account (FHSA)

The First Home Savings Account (FHSA) is a new registered savings plan in Canada designed to help Canadians save for their first home, combining the tax benefits of an RRSP and a TFSA. Here’s how it works and why it could be beneficial if you buy a home.

Benefits of the FHSA

-

Tax Deductible Contributions:

Similar to an RRSP, your contributions to an FHSA are tax-deductible, which can lower your taxable income and reduce the tax you owe. -

Tax-Free Growth:

Any investment income generated in the FHSA, like from mutual funds, stocks, ETFs, or savings accounts, is tax-free while it remains in the account. -

Tax-Free Withdrawals:

When used for buying a qualifying home, withdrawals from the FHSA are tax-free, much like a TFSA. This makes it a highly efficient way to save for a down payment.

Eligibility for Opening an FHSA

To open an FHSA, you must:

-

Be a Canadian resident who has reached the age of majority in your province or territory.

-

Be a first-time homebuyer, which means you have not lived in a home you owned, individually or jointly, in the current year or the past four calendar years.

Contribution and Withdrawal Limits

-

Contribution Limits:

-

Annual limit: $8,000, including any funds transferred from an RRSP

-

Lifetime limit: $40,000

-

Any unused portion of the annual contribution can be carried forward, allowing you to contribute up to $8,000 in any one year

-

-

Usage Period:

You must use your FHSA contributions within 15 years of opening the account, or before age 71. After that, you can transfer the savings into an RRSP or RRIF without penalty, or make a taxable withdrawal. -

Qualifying Withdrawals:

There’s no maximum on how much you can withdraw tax-free, provided you use the funds for a qualifying home. You may also be able to access your RRSP under the Home Buyers' Plan for the same home purchase.

Who Qualifies as a First-Time Homebuyer?

You qualify as a first-time homebuyer if you haven’t lived in a property you owned in the past 4 years or never purchased a home.

Newcomers to Canada are eligible, too, provided they have a valid Social Insurance Number (SIN) and meet the residency and homebuyer requirements.

How Does the FHSA Compare to Other Plans?

The FHSA combines features of both the RRSP (tax-deductible contributions) and the TFSA (tax-free withdrawals), making it an appealing option to save for a down payment on your first home.

With its unique blend of benefits, the FHSA could help first-time homebuyers reach their savings goals faster, making homeownership more accessible.

3. Home Buyers’ Tax Credit (HBTC)

The HBTC is a federal, non-refundable tax credit encouraging Canadians to purchase their first home.

This credit applies to properties in Canada that must be registered with the land registry office in your name or jointly with a spouse or common-law partner.

This tax credit can help ease the costs associated with homeownership, by offering a valuable reduction in your income taxes for the year of your home purchase. For those new to the market, it's an easy-to-miss credit that could save you significantly during tax season.

Who Qualifies as a First-Time Home Buyer?

You may qualify if:

- You, your spouse, or common-law partner haven’t owned a home you lived in within the last 4 years.

- You’ve never owned a home before.

- You must occupy the home as a principal place of residence no later than one year after it is purchased.

The four-year rule allows some individuals who’ve owned homes in the past to qualify if it’s been long enough since their last ownership.

Disability Exception: If you or a relative claim the disability tax credit, you may qualify for the HBTC even if you’ve owned a home recently. This also applies if you’re helping a relative with a disability buy a home to live in.

How Much Can You Claim?

-

You can claim up to $10,000 individually or split the amount with your spouse or partner, which provides a tax reduction of up to $1,500 (at the 15% tax rate). For example, each of you can claim $5000 and get a credit to reduce your income tax payable by $750.

-

The HBTC is non-refundable credit and will reduce the amount of taxes you owe by $750. It cannot be anymore then this amount— if you don't owe income tax, you won’t receive a benefit from the HBTC.

What Properties Qualify?

The HBTC covers a range of property types as long as they serve as your main residence:

- Single-family homes

- Semi-detached homes

- Townhouses

- Mobile homes

- Condos

- Units within apartment buildings, such as duplexes, triplexes, or fourplexes

- A share in a co-operative housing corporation that entitles you to own and provides an equity interest

Homes under construction also qualify if you move in within one year after closing.

4. GST/HST New Housing Rebate

The GST/HST New Housing Rebate is designed to help Canadian homebuyers recover a portion of the tax paid on buying or building a new home, substantially renovated homes, and certain other property types used as a primary residence. This rebate can ease the financial burden of new construction or major home improvements and can be used alongside the newly introduced First-Time Home Buyers’ GST Rebate.

Who’s Eligible?

You may qualify for the GST/HST New Housing Rebate if you’re an individual who:

- You purchased a new or substantially renovated house (building and land) from a builder for use as your or a close relation’s primary place of residence

- You purchased a new or substantially renovated mobile or floating home from a builder (this includes the manufacturer or vendor) for use as your or your relation’s primary residence.

- You purchased a share of the capital stock of a cooperative housing corporation (co-op) where the co-op paid tax on a new or substantially renovated house, as your or a relation’s principal residence

- You purchased a new or substantially renovated house from a builder where you leased the land from that builder under the same agreement to buy the house and the lease is for 20 years or more or gives you the option to buy the land

- Build or substantially renovate your own home, or hire someone to do it, for use as your or a relation’s primary residence. The fair market value of the home at substantial completion must be under $450,000

What You Can Claim

The rebate allows you to recover a portion of the GST or the federal part of the HST. The amount varies based on the home's value:

-

Homes up to $350,000 may qualify for the maximum federal rebate of 36% of the GST, up to $6,300

-

Homes between $350,000 and $450,000 may qualify for a partial rebate

-

Homes over $450,000 do not qualify for the GST/HST New Housing Rebate but may still be eligible under the First-Time Home Buyers’ GST Rebate (FTHB GST Rebate) introduced in 2025

Provincial new housing rebates may also be available on top of the federal portion, even if you don’t qualify for the full GST rebate.

What’s New – FTHB GST Rebate Can Be Combined

If you’re a first-time homebuyer, you may also be eligible for the new FTHB GST Rebate introduced in 2025. When applicable, the FTHB GST Rebate and the GST/HST New Housing Rebate can be combined, providing up to 100% of the GST back on homes valued up to $1 million.

For homes priced between $1 million and $1.5 million, the FTHB GST Rebate is reduced on a sliding scale (e.g., $25,000 rebate for a $1.25M home). No rebate applies above $1.5 million. Both programs are only available to individuals, not corporations or partnerships.

Required Documentation

To apply for the GST/HST New Housing Rebate, you'll typically submit the required tax form, along with your home purchase agreement or construction invoices. While you generally don’t need to send supporting documents right away, you must:

-

Keep all original invoices in your name (or your co-owner's name) for six years

-

Ensure that invoices are not estimates, quotes, or statements

-

Provide proof of occupancy if CRA requests it

If your builder didn’t charge GST/HST on your invoice, you’ll need to submit photocopies of those invoices with your application.

5. First-Time Home Buyers’ GST Rebate (FTHB) on New Builds

As of May 27, 2025, the federal government introduced a First-Time Home Buyers’ GST Rebate (FTHB GST Rebate) that provides significant tax relief for eligible buyers of new homes. This new rebate is designed to lower upfront costs for young Canadians and stimulate new home construction across the country.

What Is It?

The FTHB GST Rebate offers eligible first-time buyers a full GST rebate on new homes priced up to $1 million, and a partial rebate on homes priced between $1 million and $1.5 million. The maximum rebate amount is up to $50,000.

Who Qualifies?

To be eligible, at least one purchaser must:

-

Be a first-time homebuyer (not have owned or lived in a home they or their partner owned in the current or previous 4 calendar years),

-

Be at least 18 years old,

-

Be a Canadian citizen or permanent resident,

-

Intend to use the home as their primary place of residence, and

-

Be the first occupant of the home.

What Types of Homes Are Covered?

The rebate applies to,

-

New homes purchased from a builder (including on leased land),

-

Owner-built homes (including contractor-built on owned or leased land), and

-

Shares in a cooperative housing corporation, where the buyer will occupy the related unit.

Rebate Breakdown,

-

100% GST rebate on new homes priced up to $1 million,

-

Partial rebate on homes between $1 million and $1.5 million (e.g., $25,000 rebate for a $1.25M home),

-

No rebate for homes priced at or above $1.5 million.

Timeline for Eligibility

The FTHB GST Rebate is available if,

-

The purchase agreement is signed on or after May 27, 2025, and before 2031, and

-

Construction begins before 2031 and the home is substantially completed before 2036.

For Owner-Built Homes,

-

The same price and residency rules apply.

-

The rebate can recover GST paid on construction costs (materials, labor, etc.) up to a maximum of $50,000.

Co-Operative Housing Purchases,

-

Applies if you purchase a co-op share tied to a unit you intend to live in as your principal residence.

-

Not available if the co-op receives the full GST rebate for rental housing.

Important Limitations,

-

You can only claim the FTHB GST Rebate once in your lifetime.

-

If your spouse or common-law partner has previously claimed it, you are ineligible.

-

Assignment sales are not eligible unless the original agreement was signed on or after May 27, 2025.

-

Cancelling and re-signing a pre-existing agreement will not qualify you for the rebate.

Why It Matters

This rebate could save you up to $50,000 on a new home, substantially reducing the upfront financial burden and making newly built homes more accessible for first-time buyers in Manitoba and across Canada.

6. First Time Home Purchase Program (FTHPP)

The First Time Home Purchase Program (FTHPP), available to citizens of the Manitoba Metis Federation (MMF), was created to address the housing needs of its citizens in rural and urban areas.

It is delivered through the Louis Riel Capital Corporation (LRCC) and meant to provide homeownership opportunities where citizens might not have otherwise had.

This program offers:

-

5% towards the down payment - this amount is based on the home purchase price and cannot exceed $18000.00

-

1.5% towards closing costs (legal, land transfer tax etc) - this amount is based on the home purchase price and cannot exceed $2500.00

For a list of full eligibility requirements and criteria for participants, the application can be found at the following, https://www.mmf.mb.ca/first-time-home-purchase-program

Eligibility Requirements

-

Residency: Applicants must have lived in Manitoba for at least six months.

-

Métis Citizenship: Proof of Métis citizenship, either through an MMF Métis Citizenship Card or an acknowledgment letter from MMF, is required.

-

Age and Mortgage Qualification: Applicants must be 18 or older and eligible for a mortgage from a recognized financial institution. LRCC or MMF may review the terms of the mortgage.

-

Priority Groups: Priority is given to applicants in social housing or those escaping abusive situations.

-

Forgivable Loan Positioning: The forgivable loan must be registered as a second mortgage, with costs borne by the applicant.

-

Primary Residence: The property must be the applicant's primary residence, and they must not have owned a home before.

-

Real Estate Ownership Limits: Applicants must not own real estate valued over $30,000.

-

Income and Asset Limits: Annual household income must be below $100,000, and combined liquid assets must not exceed $60,000.

Eligible Home Types

-

New Builds: Homes with a new home warranty purchased as turnkey (not under construction).

-

Resale Homes: Single-family, duplexes, townhomes, condos, or multi-unit dwellings.

-

Ready-to-Move Homes (RTMs): Must be on permanent foundations.

-

Conversions: Non-residential buildings converted to residential use with a new home warranty.

-

Mobile Homes: Only on owned land, with a permanent foundation acceptable for mortgage financing.

Financial Guidelines for Home Purchases

-

Maximum home purchase price: $600,000.

Ineligible Home Types

-

Life-Lease Communities: Homes within life-lease arrangements.

-

Homes on Leased/Rented Land: Mobile homes in trailer parks.

-

Self-Built or Progressive Build Projects: The program does not cover self-built or progress-draw homes.

7. The Rural Homeownership Program

8. Manitoba Tipi Mitawa (MTM) Homeownership Program

The Manitoba Tipi Mitawa program is a partnership initiative between the Assembly of Manitoba Chiefs and the Manitoba Real Estate Association (MREA).

It offers homeowner education and financial support to Manitoba First Nations families who are first-time home buyers.

Program Overview

With its comprehensive support, including financial assistance, educational resources, and flexibility in neighborhood choice, the MTM program is a valuable pathway to homeownership for First Nations families in Manitoba. Guidance through essential steps include:

-

Financial Education – Understanding budgeting, savings, and credit.

-

Home Maintenance Training – Learning how to care for a home.

-

Realtor Selection – Choosing a REALTOR® to help with the home search.

-

Home Purchase Support – Assistance through the purchase process.

Eligibility Requirements

To qualify for the MTM program, applicants must meet the following basic criteria:

-

First-Time Homebuyer: The applicant must be buying a home for the first time.

-

Residency and Background:

-

The primary applicant must be a member of a First Nation.

-

Have lived in Manitoba for the past 10 years.

-

Agree to undergo a voluntary credit report check.

-

-

Employment and Income:

-

Must have been continuously employed full-time for at least two years.

-

Annual household income should range between $50,000 and $84,600, excluding social assistance.

-

-

Household Dependents: The applicant must have dependents living in the household, such as a person under the age of 22, or a person under the age of 26 who is registered in full-time study, or a person of any age who is recognized as a dependent of someone in the household for income tax purposes

-

Commitment to Education:

-

Must attend approximately 40 hours of educational sessions on financial literacy, home maintenance, and home purchase orientation.

-

-

Home Purchase Requirements:

-

Be willing to buy a home (minimum two bedrooms) within Winnipeg or Brandon or another major urban center.

-

Use a registered member of the Canadian Association of Home and Property Inspectors (CAHPI) for mandatory home inspection.

-

Request a Property Disclosure Statement from the seller.

-

-

Public Relations Participation: Willingness to participate in public relations for MTM.

-

Minimum Deposit: Must have at least $5,000 available for the home deposit.

Selection Process

Eligibility is assessed based on creditworthiness, which includes:

-

Income: Consistent income within the program’s specified range.

-

Credit History: Positive credit score and manageable debt ratio.

Program Financial Support

-

Maximum House Price:

-

Up to $250,000 for homes in Winnipeg and Brandon.

-

Up to $225,000 for homes in other communities.

-

-

Down Payment Assistance:

-

The program provides a 15% down payment:

-

10% is funded by the Manitoba government.

-

5% is funded by Manitoba Tipi Mitawa.

-

-

-

Legal and Closing Cost Assistance:

-

The program offers up to $4,000 to cover legal fees and closing costs, helping reduce upfront costs for first-time homebuyers.

-

Categories

Recent Posts

Leave a Reply

REALTOR®

REALTOR®I became a REALTOR® because I truly enjoy helping people find the place that feels like home and because providing exceptional service during such an important moment in someone’s life is something I genuinely care about. Supporting sellers as they move on, move up, or move forward is just as meaningful, and being part of that transition is something I’m grateful to contribute to.

I make the buying or selling journey feel organized and approachable with clear communication and practical guidance. With an approach supported by market data, trends, and neighbourhood insights, you'll always understand what’s happening and how to make the most informed decisions.

Whether you’re buying your first home, selling a place filled with memories, or planning your next step, I’m here as someone who listens, shows up, and puts your goals at the centre of every decision. I'm focused on what serves you best and I make your best interests my TOP priority.

I'm Tara Zacharias, a real estate salesperson located in the vibrant city of Winnipeg. Thanks for stopping by and taking the time to get to know me!+1(204) 293-0933 tara@tarazacharias.com330 St Mary Ave, Winnipeg, MB, R3C 3Z5, CAN

https://tarazacharias.com/